The ABS methodology is the default source for how the media and government measure and discuss Australian unemployment. Yet, these measures are arbitrary and contrived by Capital to misrepresent the true state of affairs. Note, for example, how the default description is always in terms of percentages against a rarely explained or estimated amorphous labour-force base and never in absolute numbers. Percentages rather than absolute numbers are a means of camouflaging the rising unemployment numbers in the Labour force.

In Australia, the absolute number of jobless people, as reported by the ABS, has been consistently climbing since late 2022, following the post-pandemic decline. ABS is not the only measure of unemployment as a metric of the concept of “individuals without compensated employment or secured income via a job”. How you arbitrarily define that concept can exclude or omit numerous individuals from the tally of the unemployed.

The ABS methodology incorporates many arbitrary criteria for unemployment, and is constrained by institutional structures, which, if modified, would completely change both the absolute number and ratio. This also applies to what is and isn’t considered the base “Labour-force”, against which the ratio is measured. An individual’s inclusion or exclusion from these estimates are determined solely by a nation’s adherence to, or interpretation of, a series of methodological guidelines established by the International Labour Organisation. Any shift or deviation in a nation’s methodology, yields different results.

For example, determining the definition of an “active job search” can change the estimated number. For instance, limiting active job searches to the past 4 weeks yields a specific unemployment number. Extending the timeframe to longer periods, although not in accordance with ILO standards, such as Italy’s 6-month search cutoffs in the North and 12-month cutoffs in the South, would yield very different amounts.

“Availability” as a criterion yields similar variations. In Europe, the unemployment definition prescribes an unemployed person as one currently available for work in the next fortnight, as opposed to the more “immediate” availability-for-work requirement imposed by Australia’s ABS. This results in divergent unemployment rates.

How a nation assesses gig “employment” under zero-hour contracts indicates what the eventual unemployment measure will be. If, like Australia, all that matters is a “job attachment”, than any gig, irrespective of any lack of hours or income, is nominated as “underemployment”. Despite the fact that it exists as productively and financially indistinguishable from unemployment.

A country’s unemployment inclusion, is solely determined by these prescribed regulations and the class for which those guidelines are established. The unemployment rate is based on the cut-off specified within the methodology and the demographic it is intended to serve. “For whom the bell tolls” (to cite John Donne) is significant — and the bell tolls for class divisions in Australia. The ABS, in particular, rings its “bell” for the capitalist class.

By “capitalist class,” I refer to the Veblen Institutionalist’s subdivision of the traditional Marxian ruling class. This category encompasses enterprise owners and managers whose income is derived from profits, as they accumulate capital through asset ownership and predominantly possess the “means of production” [Pluta & Leathers, 1978, p. 128]. The statistics’ primary domestic use is to impose unimpeded access, of the working class, to the capitalist class. It is essential to recognise that ABS statistics are deliberately constructed to not encompass all individuals without paid employment. I will substantiate my argument by scrutinising the ABS methodology, some of which is furnished in their 2023 online publications.

1. The ABS data excludes individuals unable to initiate immediate employment. As Gareth Hutchens’s articles in the ABC have highlighted, it freezes out thousands of unemployed individuals.

2. Exclusions for uncompensated labour in a familial enterprise, busking or street vending. Why? Due to your engagement in other demanding tasks, you may not be instantly accessible to the Capitalist Class.

3. Banning individuals from partaking in the government unemployment programs (i.e. the PaTH initiative). Why? It is necessary to vacate such programs prior to venturing into compensated labour for the capitalist class.

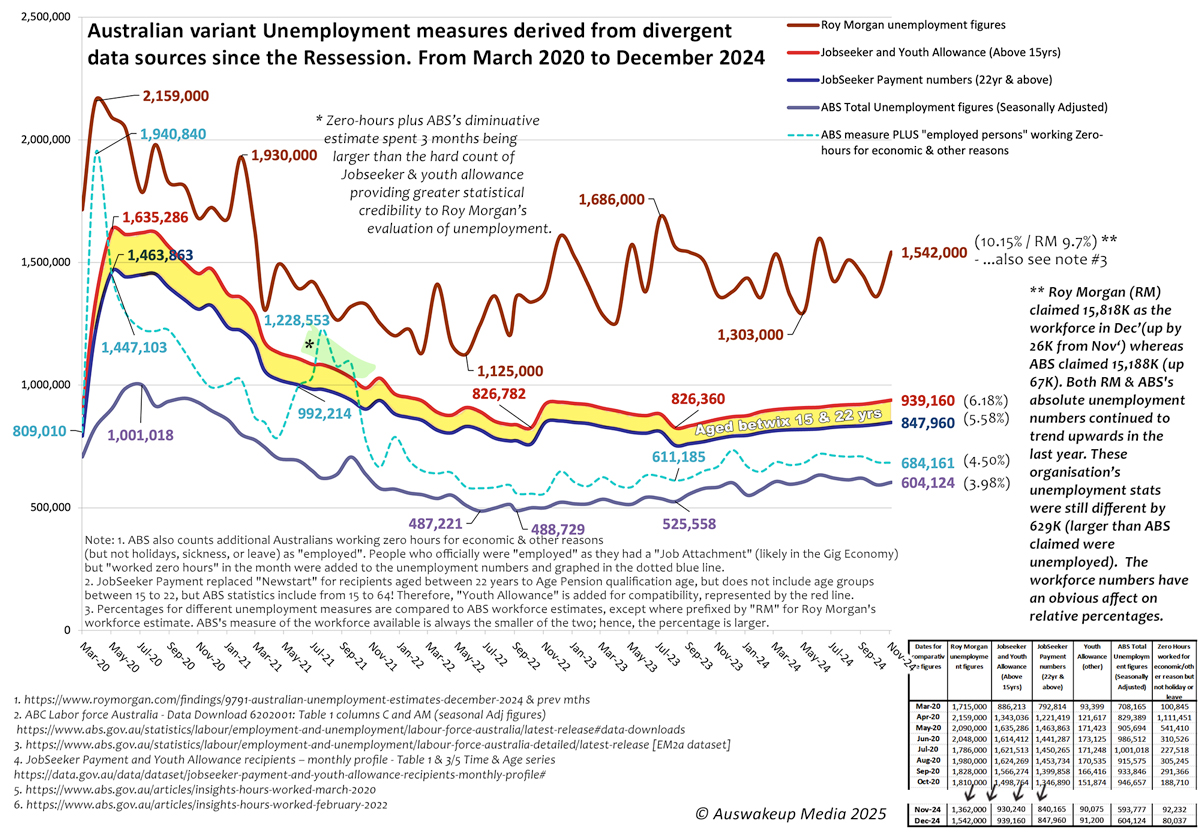

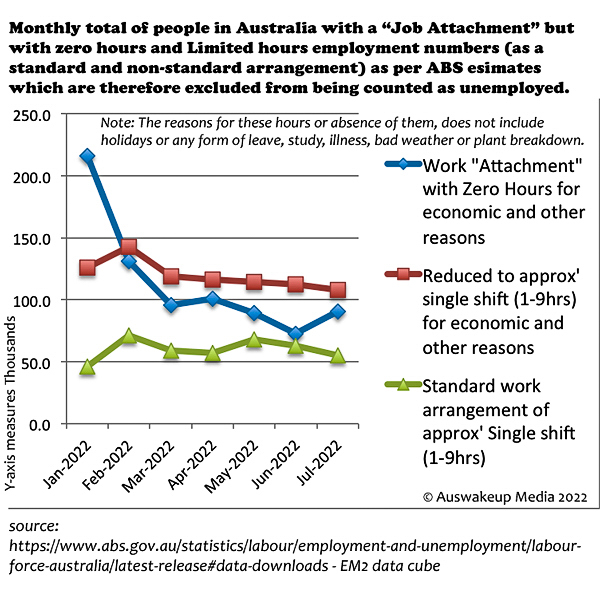

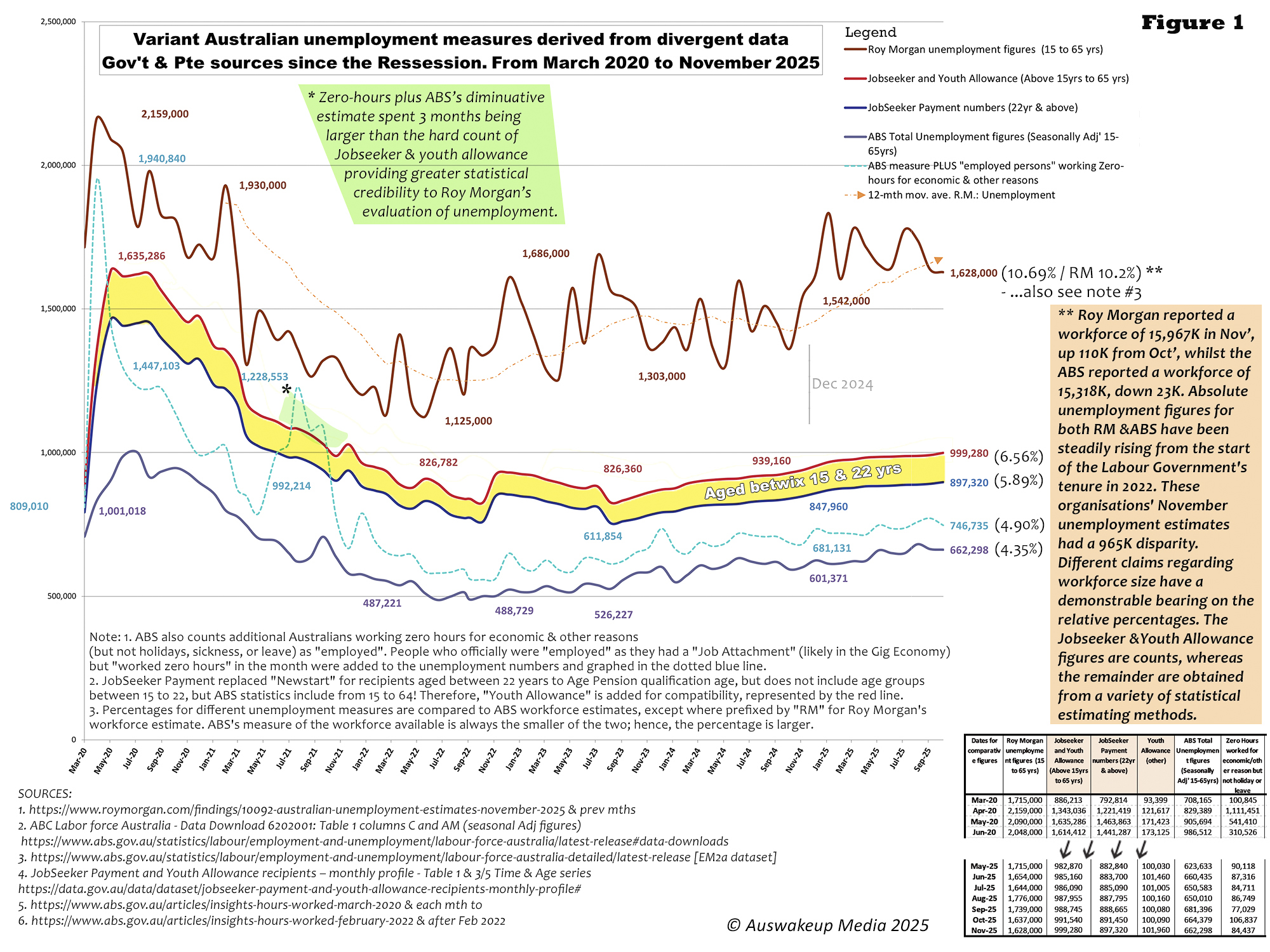

4. Excluding Australians employed for zero hours due to ‘economic reasons’ yet defending an unviable gig attachment. Why? Being earmarked to ABS’s “job attachment”, which exists as unpaid due to the absence of employment supplied, operates as an attachment obstacle to exploitation by the capitalist class. Over the course of 2025, these numbers alternated between 85K and over 100K, while in 2020, they fluctuated between 200K and over one million individuals. (see Figure 1)

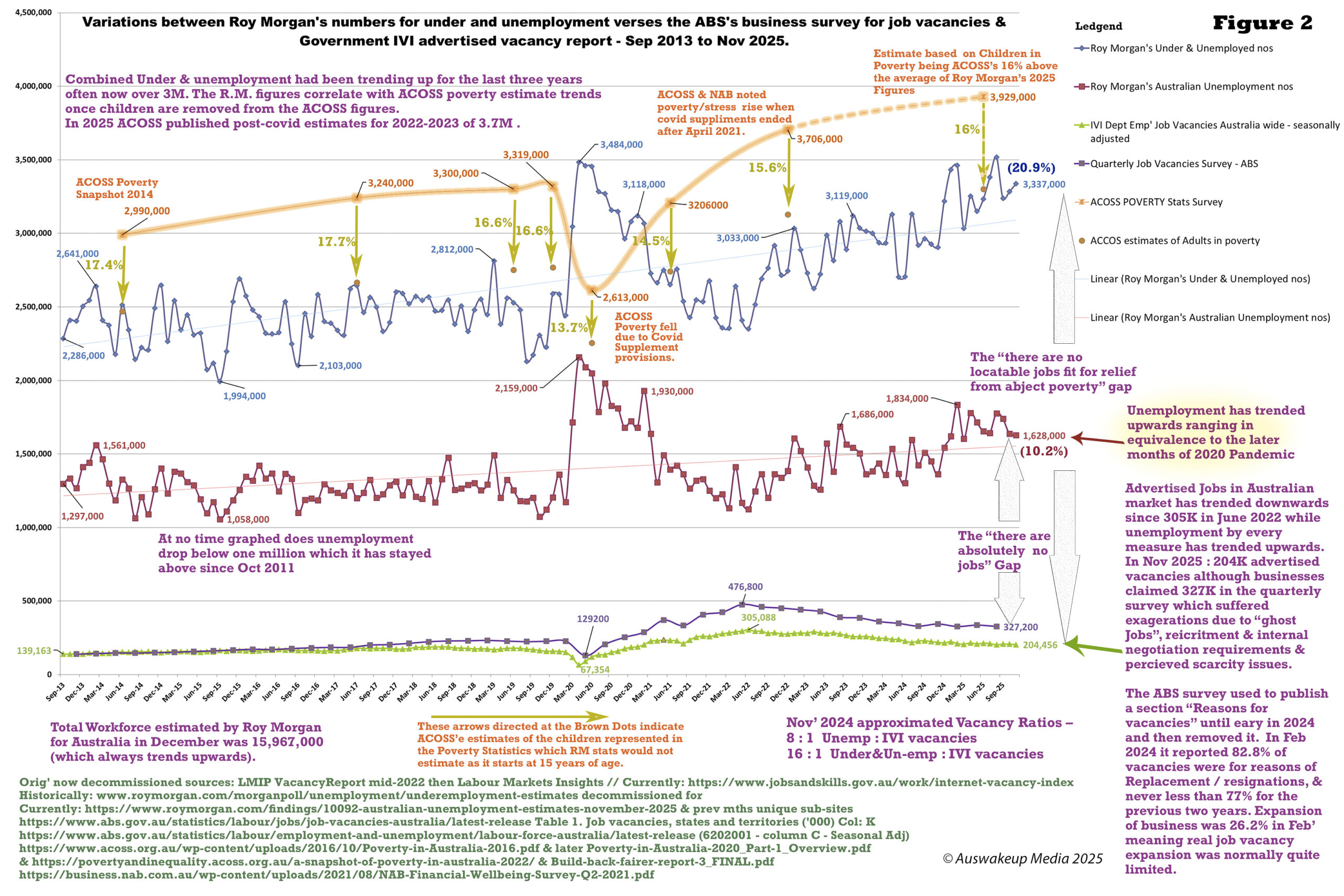

5. Excluding unemployed individuals lacking evidence of “actively” seeking employment due to familial, personal, or other obligations, irrespective of the absence of regional job vacancies. Why? To feign that the capitalist class always has adequately compensated jobs available for working-class engagement. (see Figure 2)

6. Exclusions of transient foreign individuals in the country pursuant to the 12/16 regulation. Why? A lack of familiarity with the culture, work, and social environment can hinder the working class’s full assimilation into capitalist employment management.

7. Excluding those who any other entity has employed, for over one hour within a month. Why? During the designated “reference week” or the four weeks preceding its end, you were not available for exclusive employment by anyone in the capitalist class.

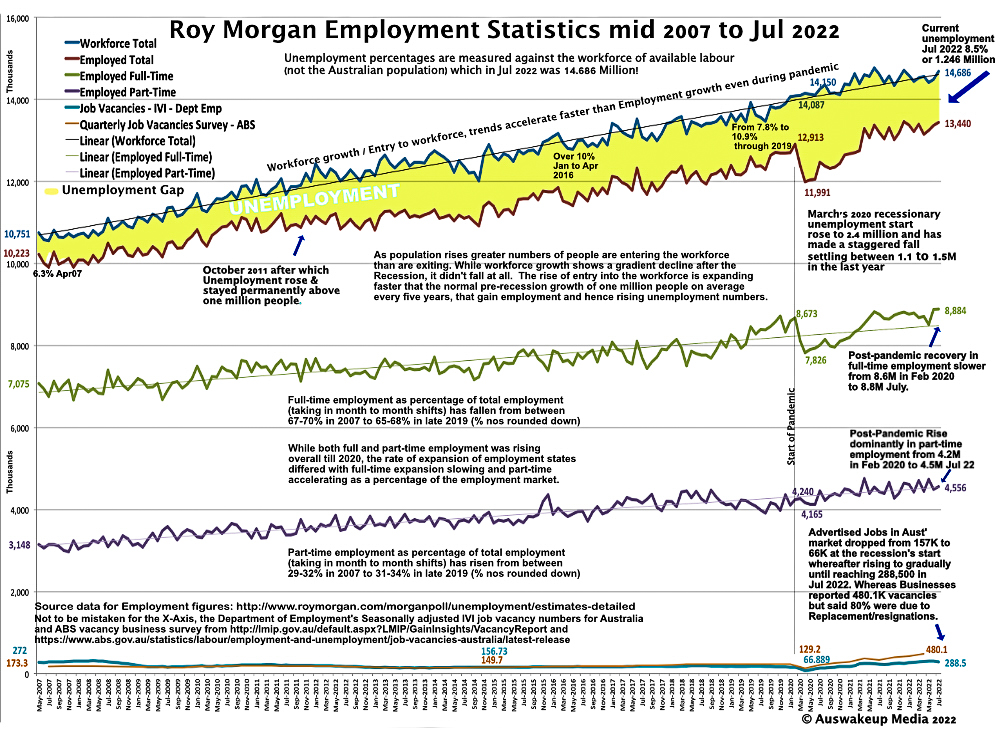

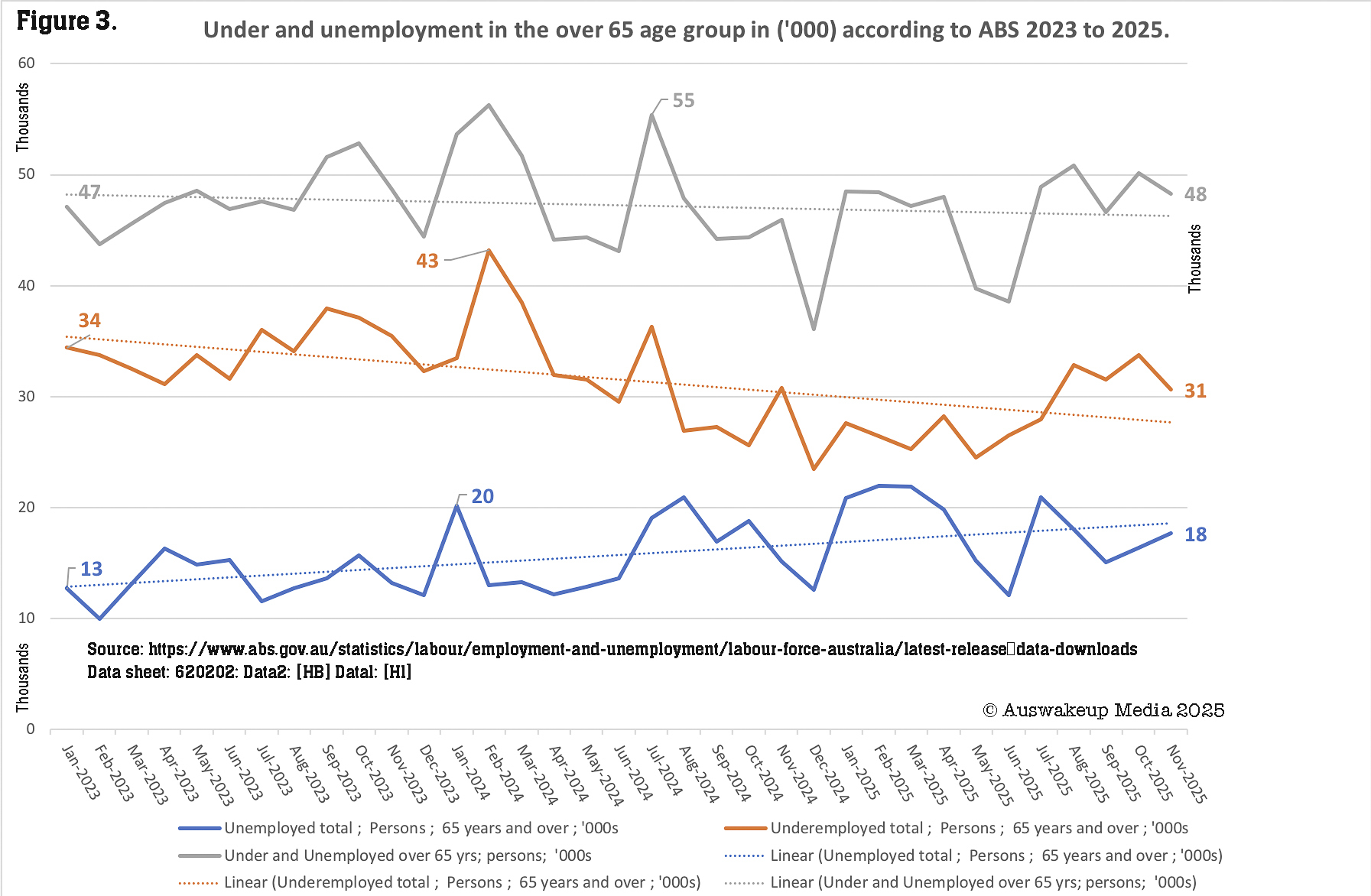

8. Excluding anyone over the age of 65, regardless of their active job-seeking status (See Figure 3). Why? Your age, physical ability, and other factors may restrict your potential for complete exploitation by the capitalist class. We live with “ageist” discrimination that disregards individuals long before they attain 65 years, regardless of their experience or abilities.

ABS measures encompass an arbitrary subset of “real unemployment”. One where people are not only unemployed but also lack any source of income (outside government welfare or family support) and are subject to a list of exclusions. This subset is constrained by age limits, active job-seeking behaviour, immediate availability, the absence of distractions, and the absence of any potential impediment to engagement in capitalist exploitation at any time. That is a vastly limited subset.

Its size is unfailingly a half to one-third smaller than the physical count of individuals to whom the Australian government disburses unemployment welfare (JobSeeker and Youth Allowance). I should also note that the number of individuals compensated by Jobseeker has increased since mid-2023, despite penalties banning thousands of people.

When confronting media and politicians’ statements, such as those by Jim Chalmers and members of the Labor cabinet, in multiple Twitter messages, claiming “unemployment is low,” I would argue that this is entirely misleading. Irrespective of whether it is reported intentionally, naively, consciously, or otherwise, it is misleading. When regurgitating that absurdity, give sceptical contemplation to the agenda and propaganda of the capitalist and ruling class. It also has consequences for the employed, including affecting the RBA’s Taylor Rule and prompting inflationary interest rates. Is there a more accurate depiction of unemployment that furnishes a more accurate assessment of individuals without compensated employment?

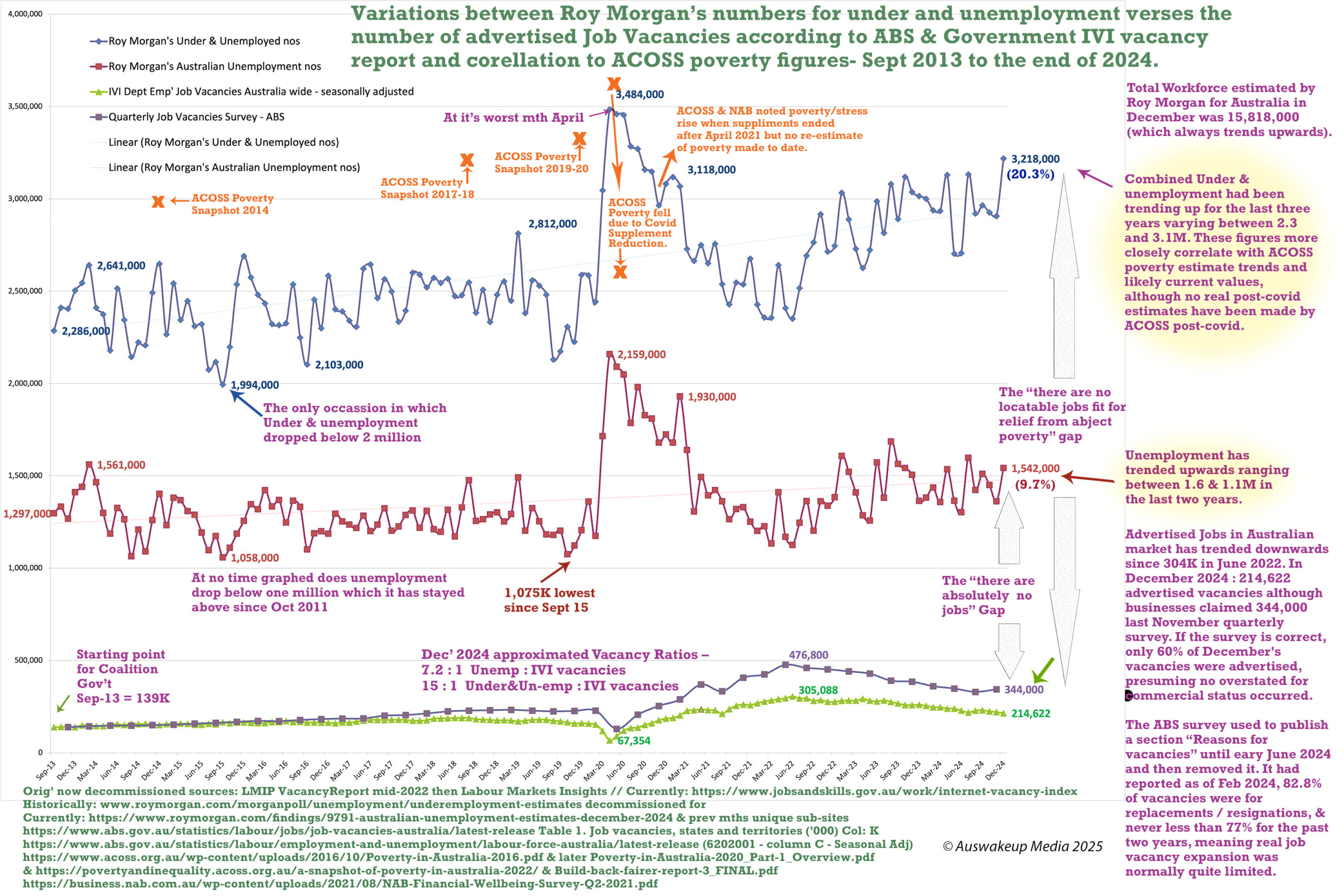

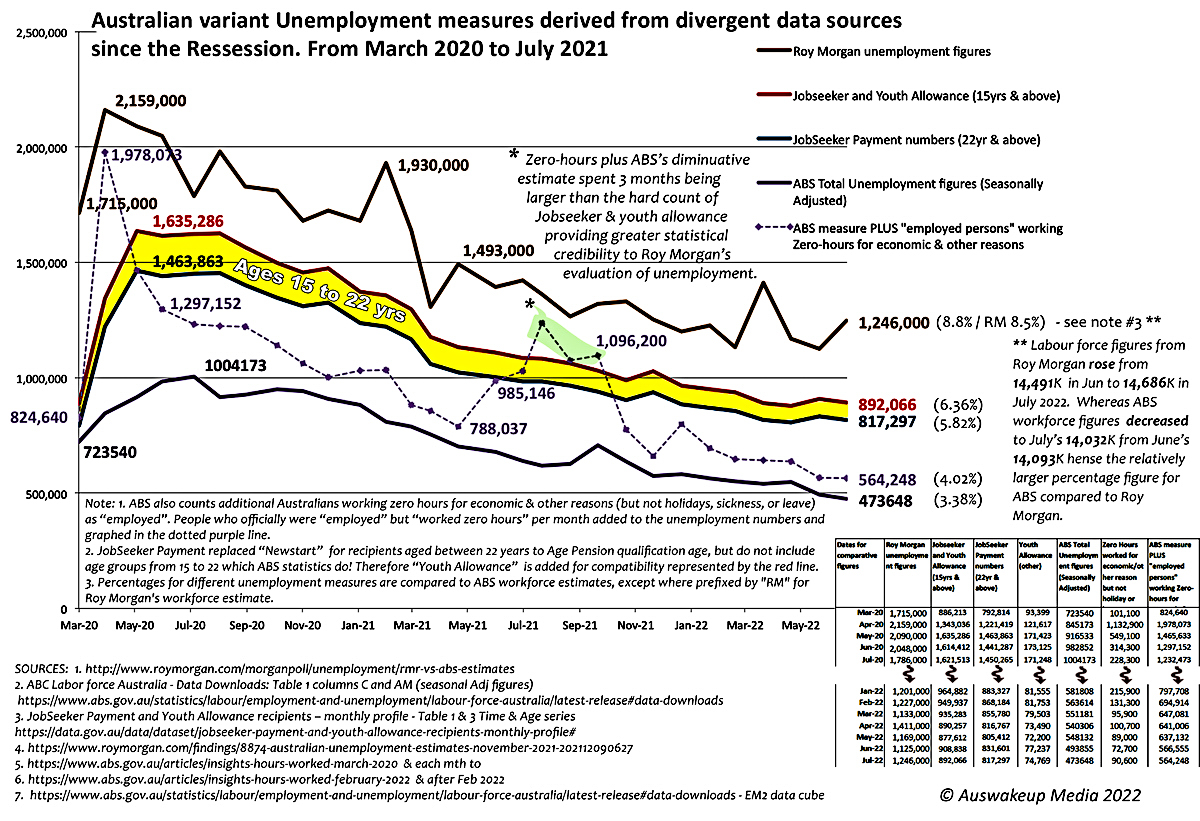

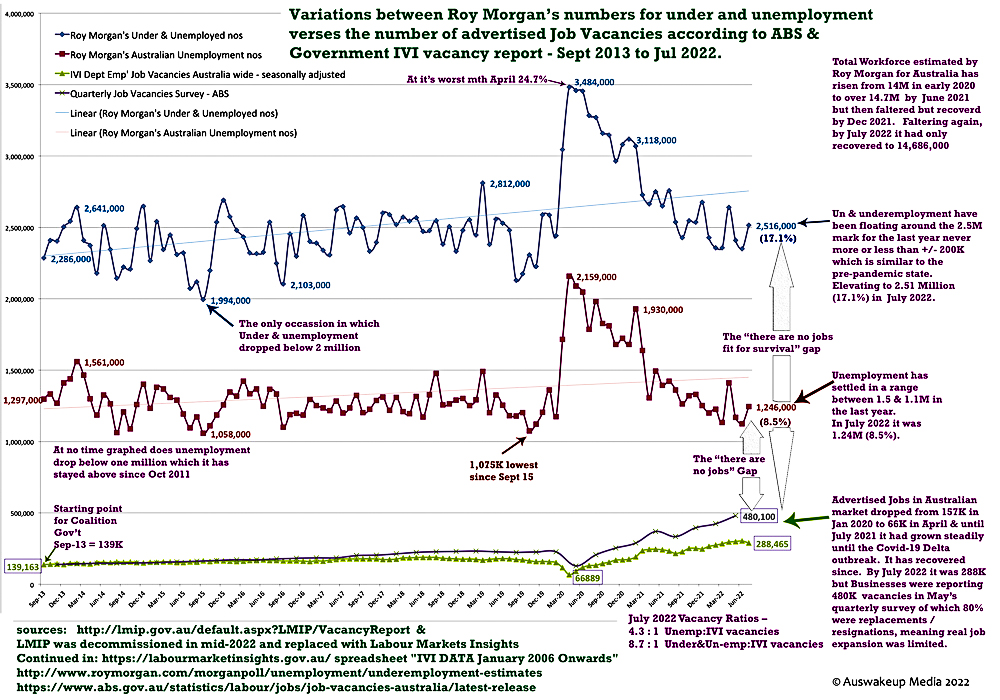

Investigate the results of Roy Morgan’s methodology, exemplified in Figure 2, and consider its relative correlation to past poverty measures by ACOSS. Including my prediction for the last figure, based on the likely prevalence of child poverty, to determine it’s likely to be close to 4 million. Children under 16 are not factored into any unemployment measure, so poverty figures will always be larger than under and unemployment aggregates. Over the last decade, ACOSS has found, that child poverty is within 2 percent range of 16%, except once when the government raised unemployment welfare above poverty levels. It should be noted that the roughly 1.5 million that ABS claims is its underemployment and unemployment aggregate total has no reasonable correlation with poverty figures that can be explained by children, rendering it highly unrealistic.

Roy Morgan insinuates that Australia’s unemployment rate has been in double digits for most of the year to date. The combined unemployment and underemployment rate has floated above 20% and is more closely correlated with ACOSS’s independent poverty figures. But even were one to be naively constrained to accept ABS figures, there is no denying that — like Jobseeker payments and Roy Morgan — unemployment has been trending upwards in absolute numbers ever since Labor came into power.

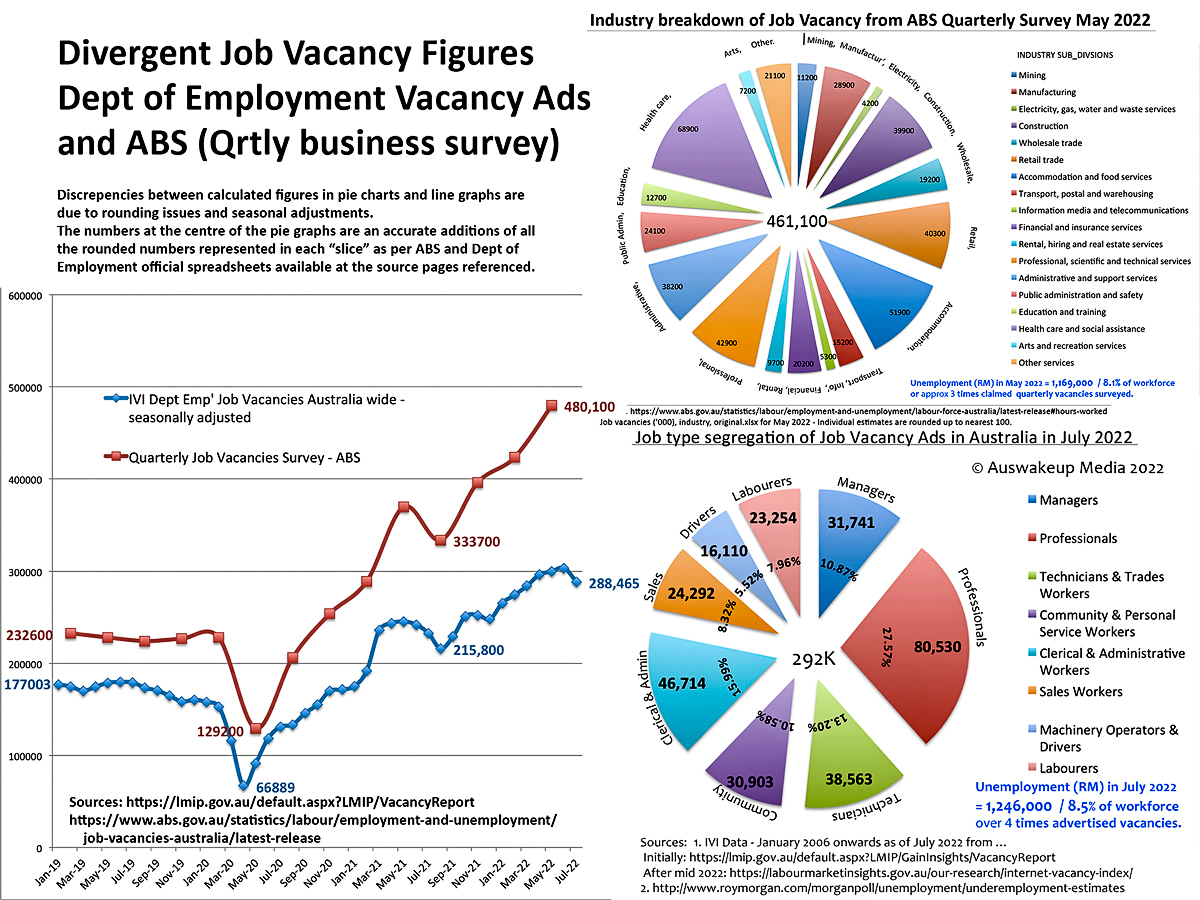

Further to the issues of unemployment, a cursory examination of Figure 2’s two measures of job vacancies (with their own issues with arbitrary measurement) and those originating from distinct governmental sources and methodologies is woefully inadequate for our employment needs. Worse still, as unemployment is rising by every apparent measure, job vacancies are falling by every applicable measure. This is our economic malaise, about which next to nobody in the media is conceding.

While the present government may have exemplified greater political stability than the preceding decade of neoliberal conservative rule, which was characterised by dysfunction, corruption, and scandals under the Liberals, it is still, in itself, only marginally less neoliberal and conservative. Irrespectively, it remains suboptimal for the literal millions in Australia suffering from poverty, which ironically, the Morrison Government demonstrated it could alleviate. Yet unemployment has not improved, regardless of the methodology one prefers, and the government refuses to intensify its efforts to rectify this situation, as “state capture” guarantees its capitulation to the capitalist class.

There are solutions such as a “Federal Job Guarantee”. Although that will face vehement opposition from the capitalist class (Hail, 2021). We should minimally advocate for “Full Employment” policies reminiscent of those that resulted in less than 2% unemployment for most of the 25 years following Prime Minister John Curtin’s initiative. At a minimum, we must banish corporate and political rhetoric, no matter our political affiliations, that claims Australia has low unemployment.